*Hero*

The Herotoken Banking Concept using Blockchain Technology

The essence of creating credit facilities and loans is to enable the establishment of a functional banking system and a structured one at that. This is the foundation through which great businesses are harnessed and developed for the creative process of ventures and enterprises. Banks are thus there to enhance and enable this structure in making such means a welcome development for the people in essence. The driving force of this structure is the defining factor which enables all the main reason Herotoken is established. The Herotoken is the future of Banking in South-East Asia. This platform through the token sequence hopes to shape the old banking system by its new revolutionalized decentralized system by using blockchain structure and the token niche in building such an enterprise.It is a tremendous structure built around the transparencies and financial sustainability for harnessing growth of individuals financial and their businesses. This is the main reason why Herotoken has come to stay. It navigates on the future hopes financially of businesses in South-East Asia. This tend to provide the affordable needed credits all small medium enterprises need. It therefore, tends to provide the benefits of such a decentralized system created for sharing and making the South-East Asian business person or corporation benefit tremendously from the blockchain technology framework. This is an interesting and exciting new way of accessing credits and loans for all business people who have explored options of accessing such credits but to no avail.The Herotoken provides the enabling leverage for meeting all credit options needed in supporting businesses and also growing them generally. This in effect provides the viability and mobility of currency sharing and transactions been carried out on the platform for investors and users. The greatest pointer and benefit this draws on all levels within the context of banking lies on the possibility of accessing loan facilities without a lot of constraints.

Secondly, the Herotoken platform through its Blockchain Platform and framework develops a system which creates the avenue for people to have flexible and reliable bank accounts through the Herotoken revolutionalized way. This way propels on the blockchain technology framework adopted for this purpose of making banking process affordable and easy for investors, users and simple people that just need to bank, will freely access blockchain based loans without collaterals in exchange of different tokens. This is in essence the captivating and most flux formal platform globally acclaimed for spreading its process from the South-East Asian business person to anyone around the world. It hopes and shapes to be exemplary for other banks to follow suit. The principle reason for this approach will shape the world for better, when access to loans and credits is made readily available through such a transparent and trustworthy platform of banking paradigm. This provides in essence the easiest and most effective way banking should be done and mostly with the scalability and availability of credits. The value of one Herotoken is about 0.005 Ethereum. This provides the enabling investors opportunity for all to partake in the crowdsale purchase. All, people or prospective users and investors need to do is access the purchase of tokens on the website https://herotoken.io .Thus, on the platform will accessibility and also availability of other informations can be made available and better communicated. This is why Herotoken stands out and will continuen successively. Thus, invest and change your life dreams in accessibility and achievements. It is a welcomed development.

Market Overview

Southeast Asia is the world’s fastest growing Internet region. With 260 million Internet users out of a population of more than 600 million people, it is the 4th largest Internet market in the world. By 2020 Internet users in the region are expected to reach up to more than 480 million users, led by Indonesia, the world’s fastest growing Internet market. Unsurprisingly, the growth is anchored by the region’s thriving young population, with 70% of the (against China’s 57%) population comprised of those under 40.[2] A study made by Google and Temasek predicts that by 2025 the South East Asian Internet economy is expected to reach 200 Billion USD, strengthening its already strong and growing GDP of 2.5 Trillion USD.[3] With its mobile connection rate higher than the global average, (124% vs. 103%) and its Internet speeds expected to reach the global average of 23.3 mbps soon, the region’s Internet industry is flourishing. Furthermore, as of January 2017, social media penetration of its member countries is high. In the Philippines it stands at 58%, higher than the global average of 37% and the regional average of 47%.[4] Yet only 27% of the South East Asian population has a bank account. In poor countries like Cambodia the numbers fall to about 5%. That’s about 438 million people in the region unbanked.[5] The Philippines has one of the lowest banking penetration rates in Asia, with over 70% of adults (aged 15+ years) unbanked. Central bank data suggest that outside Metro Manila, the unbanked comprise more than 80% of the population, and only 3 million households have a credit card. As a result, 72% of the its more than 100 million population depend on more than 18,000 pawnshops for their cash needs.[6] With 90% of pawnshop customers in the country belonging to this unbanked population, pawnshops serve as their banks. Unlike the US, this is common for emerging markets like the Philippines. However there’s a problem with the traditional pawnshops that the unbanked population rely upon. It is their unreasonable interest rates that can reach over 100% per year, making it impossible for people to redeem their collateral and improve their already grave financial situations. These places mainly accept jewelery as collateral, something most young people don’t have. And while there are a lot of pawnshops, most of the unbanked Filipinos spend hours on the road, “shopping around” for the best deal. Being subject to one of the worst traffic situations in the world,[7] it can make the whole experience very expensive and inconvenient. (continued).

Mission and Vision

Hero’s mission is to revolutionize the banking industry to make credit more readily available and affordable for the unbanked or underbanked starting in Southeast Asia. Since 2015, we’ve helped thousands of Filipinos access short-term credit and that number is growing fast. As a pioneer in online lending in Southeast Asia, we have become one of the most distinguished Fintech startups to disrupt the highly entrenched, multi-billion dollar lending industry. Through our platform, we are already providing a revolutionary solution to a significant problem among the unbanked and underbanked across emerging markets. Headquartered in Singapore, we fully operate online with no branch infrastructure, allowing us to keep operating costs low and to stay focused on our customers. We are transforming lending into a frictionless, transparent, and highly efficient digital experience for Southeast Asia. Our vision is to disrupt the current financial system that excludes 2 billion people from the banking system by leveraging technology to create a more inclusive system that allows people access to credit.

Solution

“Banking is necessary, banks are not.” — Bill Gates Uber has nothing to do with cars, but it created an entirely new transportation experience. The value of having a physical network is diminishing — especially a traditional branch network.[9] Branch overhead and associated staff costs make up 60–65% of a total cost base for a brick-and-mortar lending company with an extensive branch network. Moreover, roughly 60–70% of employees are doing manual process-driven jobs and these inefficient processes add to the cost of running a physical network. It is more error prone and there is a long process of human decisions involved. We believe banks tomorrow will look fundamentally different from banks today. But by the time they get there new entrants have a window of opportunity to innovate better value at lower cost, and create a better customer experience and Hero wants to be the one that leads that change. Introducing Hero, the future of banking that provides collateralized loans to the unbanked and underbanked consumer across Southeast Asia. With the success of this token sale, Hero intends to expand into blockchain-based uncollateralized loans. Backed by venture capitalists such as Softbank and Alibaba, the organization started operating in the Philippines in 2015 and has since helped thousands of Filipinos to obtain access to affordable credit. Our first product was launched in 2015 and is the first fully licensed online pawnshop in Southeast Asia. PawnHero essentially turns mobile phones into pawnshops. Because we don’t maintain a physical pawnshop and leverage technology, we are able to reduce interest rates by more than one half, providing access to cheaper credit that improves livelihoods. We do not limit ourselves to jewelry but also accept among other collateral electronics, watches and handbags. Filipinos no longer need to leave the comfort of their homes in order to get a loan. In the past two years, we’ve provided loans to individuals that would have been turned away by the traditional pawnshops pawnshops due to the type of collateral they pawned as well as by banks because they have no credit history. We’ve improved access to credit by using the internet and we want to scale our impact using Blockchain.

Hero Token

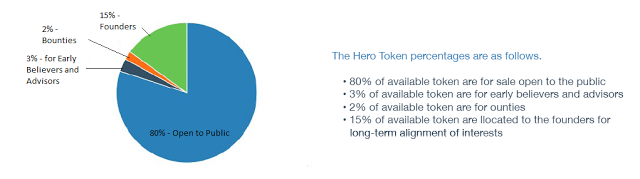

Hero token sale details On TBD at 8PM Singapore Time we will offer 80% of all Hero tokens to be created for purchase by the public in the Hero Token Sale under the ticker symbol Hero. The remaining 20% of all Hero tokens will be distributed to bounties, early believers, advisors and founders to ensure long-term alignment of interest and commitment to the tokens and their future value. Each Hero token will be sold for 1/200 ETH, meaning 1 ETH will give you 200 Hero tokens. For each token and cryptocurrency, you will receive Hero tokens in exchange, just as if you bought them with Ether or Bitcoin instead. The exchange rate that will be used to calculate this will be based on the rate of the currency or token you would like to use vis-a-vis Ethereum.

Only use the wallet address that we make available on our website at www.herotoken.io prior to the token sale.

Token Name

Hero Token (Symbol HERO) — The Future of Banking in Southeast Asia

The amount of tokens that are created for the Hero chain are all dependent on how many coins are sold during the token sale. A maximum of 250,000 Ethereum (ETH) tokens will be accepted for the purchase of Hero tokens in this token sale. The maximum amount contributed will in turn represent 80% of all Hero tokens. Since we don’t know the total that will be sold, the token sale operates based off of percentages to ensure fairness for all. Should the maximum amount be reached prior to the end of the sale on TBD, which is 4 weeks after the start of the token sale, we will cut off the token sale. In the event that such maximum amount is not fully funded by the end of the token sale, the percentage of 80% of all tokens will be adjusted accordingly, with the difference between such lower amount and the maximum amount being reserved for future token sales.

Value to Investors

Hero has been created to create both financial return and positive social impact. A Hero token represents the right to receive a reward, which is part of the interest income earned. It does not represent equity in the company nor have any intrinsic value. All tokens in aggregate will have the right to receive up to 20% of interest income. The tokens will be assigned pro rata to the fund provided during the token sale. Up to 20% of the distributable interest income is transferred to the specific Ethereum (ETH) wallet on a quarterly basis. The ETH is then redistributed to all holders of Hero tokens according to the smart contract conditions (i.e. the stake of interest income is received pro rata the share of tokens owned.) Long term Hero will strive to distribute the rewards in a shorter period of time, with the target of monthly reward distribution. In addition, the company may use a percentage of profits to repurchase Hero tokens from the open market at the prevailing market price, therefore the value of the token should be positively correlated to the success of Hero.

Hero are strategically designed to add value to the Hero network: • Reward bearing tokens — like a interest • Social impact of helping underserved access affordable credit • Buy back: The company may use a percentage of profits to repurchase Hero tokens from the open market at the prevailing market price, therefore the value of the token should be further positively correlated to the success of the project. p Value to Investors There is no risk of interest default on pawn loans granted by PawnHero. PawnHero withholds the entire interest due over the term of a pawn loan up front by deducting the interest from the proceeds credited to the customer. As an example, a 1,000 Philippine Peso (PHP) loan with a 3 month term and a monthly interest rate of 2.99% would earn 89.7 PHP of interest. PawnHero only releases 910.3 PHP to the customer and thus collects the full 89.7 PHP of interest with no risk of interest default. After the 3 month term of the loan, the customer is required to redeem the loan by paying 1,000 PHP. Depending on the underlying collateral PawnHero offers the customer to renew the loan at which point additional inte renew the loan at which point additional interest is due. Investors receive 20% of the interest collected. So that is the 20% of 89.7 PHP. For the quarterly respectively monthly distribution of interest, the sum of all loans released within the period are used.

Details Information :

Website : https://herotoken.io/

Facebook : https://www.facebook.com/PawnHero.ph

Twitter : https://twitter.com/PawnHeroPH

Bitcointalk profile: Yuni comel

https://bitcointalk.org/index.php?action=profile;u=1350925

Tidak ada komentar:

Posting Komentar